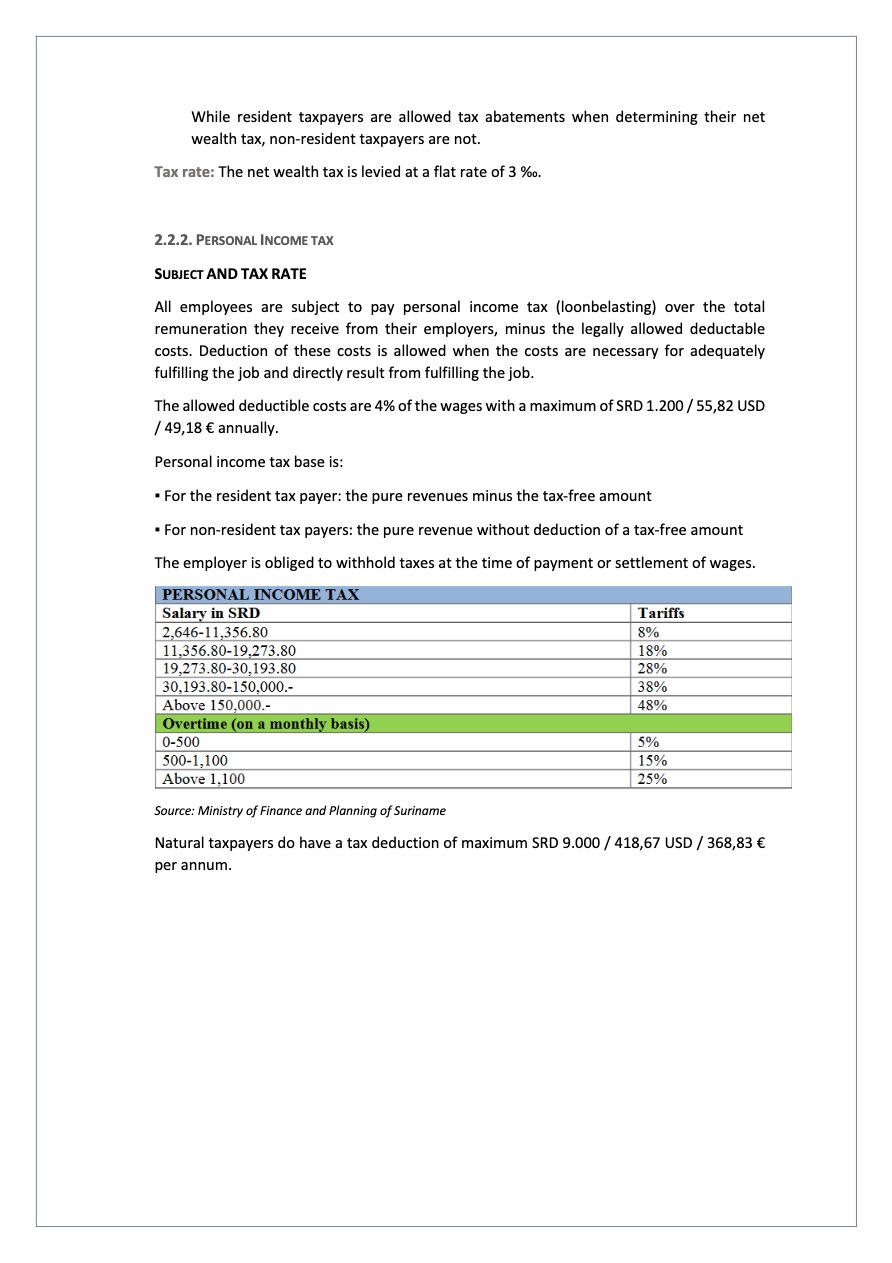

The 2001 Investment Act is the Law governing the promotion of investments in Suriname.

It grants certain incentives for entrepreneurs who keep regular accounts on their operations (with annual closings) and who, in a year, invest in operating assets intended to be used within the framework of the enterprise, as long as the business belongs to one of the key sectors for the country:

Agriculture Animal husbandry Fisheries Aquaculture Mining Forestry Tourism (*except fixtures and fitting and the operation of casinos) Industry Trade Building industry Services Road transport and haulage

Agriculture Animal husbandry Fisheries Aquaculture Mining Forestry Tourism (*except fixtures and fitting and the operation of casinos) Industry Trade Building industry Services Road transport and haulage

The main incentives in force are the following ones:

A. FREE WRITE OFFS

When computing the profit enjoyed in a year for the profit of levying income tax, the amount of the investment (in operating assets) shall be depreciated arbitrarily if:

1. Above-mentioned general conditions apply

2. The investment in Surinamese guilders is at least the equivalent of USD5.000.

3. The request for application of this facility is submitted no later than 3 months after the date of the investment concerned.

B. EXEMPTION FROM INCOME TAX

The profit enjoyed in the commencement year of an enterprise (and the following 9 years) shall be exempted from income tax if:

1. the company is new and has profit

2. the company belongs to the key sectors, namely: agriculture, livestock, fisheries, aquaculture, mining, forestry, tourism (with the exception of the establishment and operation of casinos), industry, commerce, construction, services and professional transport.

3. No claim is made on the following facilities:

arbitrary depreciation deduction of imputed interest rate Investment tax credit Group relief; and Reduction of payroll tax

4. It must be a major investment.

5. Jobs must be created with the new company.

The general requirements still apply, and the value of the capital good must meet the following premises:

– a CIF-value of USD 7.500 (unless it’s an initial investment)

– In the case of capital goods that are associated with an initial investment, the combined value should be at least USD 500.000.

– In case of capital goods which will be used in the agriculture, horticulture and poultry sector and are associated with an initial investment, exemption of

import duties is given if the total value is at least USD 250.000 USD.

The details concerning these general exemptions as well as other specific exemptions can be consulted in the flipbook HOW TO INVEST.

3.1 Forms of establishing a business in Suriname

There are different forms of establishing a business in Suriname:

However, the most common ones are sole proprietorship and limited liability company.

The details of sole proprietorship and limited liability companies can be consulted in the flipbook HOW TO INVEST.

Hire local talent

Three types of employment contracts exist:

By law, the principle of the 8.5 hour working day or the 48-hour working week is included in the Labor Act 1963, however, some exceptions to the rule exist.

The details regarding labor regulations can be consulted in the flipbook HOW TO INVEST.

Visa process information

Under working permits legislation, Surinamese law requires foreign companies to give preference to hiring nationals. Foreigners need both a residence permit and a work permit to settle in the country:

However, if employees meet some requirements, the employer is exempted from obtaining a work permit

The details regarding the permits for foreign workers can be consulted in the flipbook HOW TO INVEST.